RBA Hikes Rates to 4.10%: What Homebuyers Should Know

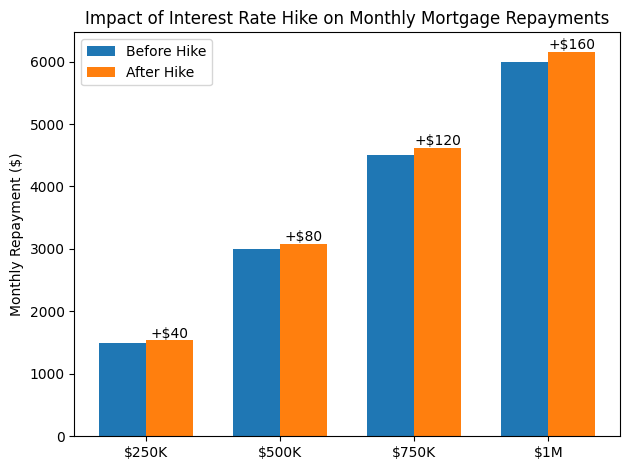

The Reserve Bank has lifted the cash rate by 25 basis points to 4.10%. Inflation fell since its 2022 peak but picked up again in late 2025, and global shocks (like the Middle East conflict) have driven fuel and goods prices higher. In short, the RBA warned that inflation risks are still “tilted to the upside” and that more hikes can’t be ruled out. For homebuyers, the immediate result is higher borrowing costs. For example, someone with a $500K loan will pay roughly $80 more per month after this 0.25% rise.

What This Means for Borrowers and Buyers

- Tighter borrowing power: Every rate rise reduces loan capacity. At D’MANSHA, we always crunch the numbers first. A $600K mortgage might cost about $90 extra per month after this hike. That’s why we tell clients to stay within their budget.

- Slower price growth: Higher rates tend to cool demand and moderate price rises. In fact, economists are already scaling back forecasts – one report sees national home prices rising only 0–3% in 2026. RBA data show housing prices grew strongly in 2025 but growth is already easing in 2026. We expect prices to keep going up in many areas, but at a slower pace. Sellers may need to be more flexible with price and terms, giving informed buyers room to negotiate.

- Strong fundamentals still at play: Our view is that the property market’s long-term drivers remain solid. Australia still faces a housing shortage, low rental vacancy rates, and steady population growth. As one industry expert noted, “Population growth is still elevated, new supply lagging and listings are tight…so there is a floor under prices”. We’ve seen investors returning thanks to tight rentals, and first-home buyer incentives continue to boost demand at the entry level..

Strategy Tips for Buyers

- Crunch the numbers first. Re-run your mortgage calculator under the new rate. Check how that extra $80–$90 per $500–$600K loan affects your monthly budget. If you haven’t already, use the Borrowing Power Calculator on our site.

- Stay calm and patient. Don’t panic or over-bid. History shows buyers remain active even as rates rise. Competition may soften, so you have time to shop around. Stick to your limit and be ready to walk away if a property is beyond it.

- Focus on fundamentals. Short-term volatility is normal; long-term value comes from good fundamentals. Look beyond hype to strong locations and properties with real upside. Compare suburbs by things like historical capital growth and rent levels. For example, some experts predict major city price gains could slow (even turn flat) but growth hotspots like Perth or Brisbane may stay strong. Our approach is data-driven: we break down metrics so our clients’ decisions are based on numbers, not nerves.

We’re Here to Help

Higher rates may be challenging, but they’re also part of normal market cycles. If you’re finding all the news confusing, remember: every buyer’s situation is unique. We at D’MANSHA take a personal, first-person approach and would welcome a chat about how the latest RBA decision affects your buying plans. Call us anytime at 0406 11 22 44 or book a free consultation through our website to discuss your goals. We can walk you through your options, suburb analyses, and negotiation strategy. Stay connected with us on Instagram and LinkedIn for the latest updates.