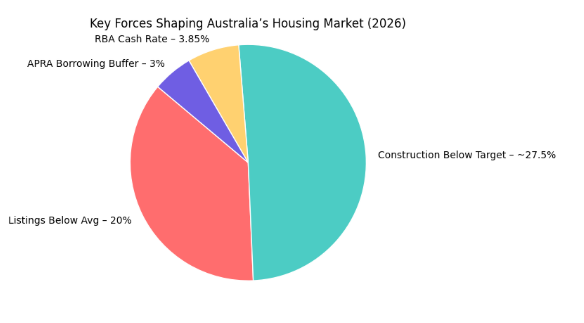

The RBA unexpectedly lifted the cash rate by 25bps to 3.85% in early Feb 2026. While higher rates and APRA’s 3% buffer might be expected to cool buyers, the reality is that a far bigger factor is supply shortage. Herron Todd White reports total listings are about 20% below the five-year average, and new home construction is running 25–30% below federal targets. In practice, this scarcity along with strong population growth and investor demand is keeping prices firm. Many buyers are now competing fiercely on smaller or less ideal homes rather than sitting out the market.

Note: Together, these four factors show that housing conditions are putting nearly 54.35% pressure on the broader economy, mainly due to supply shortages and borrowing limits.

Auctions are back in play too. Early 2026 has seen “significantly higher auction activity… and stronger clearance rates” than a year ago. This means properties sell quickly, often above reserve. For buyers, it pays to be prepared: having finance pre-approved and a clear bidding strategy is now essential. We see first-home buyers (with grants) and investors (chasing yields) duking it out in the sub-median segment. In short, low inventory is supporting prices and intensifying competition at auctions.

Growth Concentrates in Cheaper Homes

Australia’s housing market is now very much a two-speed economy. In the big east-coast capitals, Sydney and Melbourne values are flat, but in Perth, Brisbane and Adelaide, things are booming. Perth led the nation with +2.3% growth in Feb (about +27% year-on-year), thanks to listings roughly 50% below the 5-year norm. Brisbane and Adelaide also saw gains (~+1.3–1.6% each) in Feb. In contrast, stock levels in Sydney/Melbourne are only marginally below average – sellers held back earlier, but more are coming forward now. This split means smart buyers should broaden their search: the State selection strategy is important. Markets like Perth and Brisbane offer stronger upside, while Sydney/Melbourne may lead the next slowdown.

Affordability is another key theme. Growth is concentrated in the lower-priced tiers of each city. Sydney’s lower-quartile homes are up about 12.7% over the past year, versus only ~3.5% for the top quartile. Why? High borrowing costs and stretched budgets are pushing buyers down-market. In fact, Cotality data suggest a median household would need about 45% of its income for repayments on a median-priced home, well above most lenders’ comfort. And be aware of timing risk: the “two-speed” divide means east-coast prices could soften later, so avoid panic bidding in those markets.

Key takeaways for Buyers to Keep in Mind

- Supply is tight: Listings are ~20% below normal, keeping auctions competitive. Prepare to move fast.

- Auction pace: Clearance rates are up on last year; homes sell quickly once listed.

- State divergence: Perth, Brisbane, Adelaide are booming (+2–3% monthly) while Sydney/Melb are flat. Consider interstate or emerging markets.

- Lower-end focus: More affordable homes are seeing the biggest gains. First-home buyers and investors are competing here.

- Borrowing limits: Lenders factor in a 3% buffer, and many families need ~45% of income for a median loan. Plan your budget carefully.

We at D’MANSHA blend data-driven insight with on-the-ground expertise, so you don’t have to navigate this complex market alone. For personalised guidance, call us at 0406 11 22 44 or book a free consultation. We can crunch the numbers on our calculators page, review your borrowing power, and help you craft a strategy aligned with your goals. Contact us to start your smart home-buying journey today and follow us on LinkedIn and Instagram.