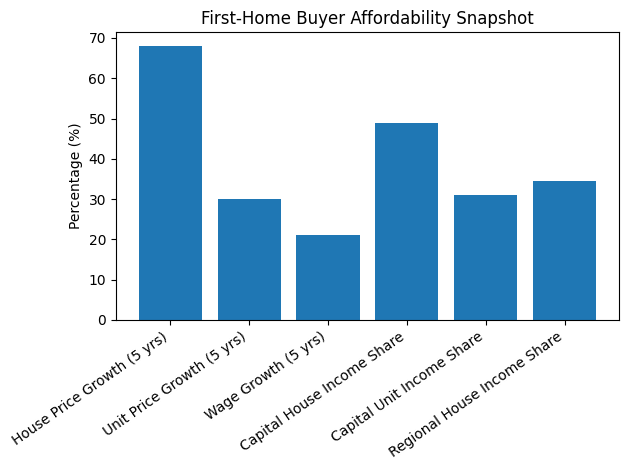

Australia’s housing market is becoming one of the toughest for first-home buyers. As buyer’s agents, we see from the latest Domain data that entry-level prices have surged while incomes lag. Nationally, entry-level house prices are up 68% over five years (units +30%), versus only 21% growth in typical wages. This means saving a 20% deposit now takes much longer – for example, about 7.7 years for a Sydney house compared to just 2.7 years for a Darwin unit. In the capital cities, entry-level homes are straining budgets: houses require roughly 49% of household income to service (compared to about 34% in regional areas), and units about 31%. In short, nearly all capital-city markets now exceed recognised stress thresholds on house loans.

Key Stats from the Report

- Prices vs Wages: In the past five years entry-level house prices rose 68% (units +30%) while wages grew ~21%. Both outpace inflation (23%).

- City Records: Sydney remains the only capital where an entry-level house tops $1 million. It saw 15% price growth last year, with buyers taking 7.7 years to save a deposit. Brisbane, Perth and Adelaide houses jumped over 20% in the last year.

- Deposit Timelines: Saving a 20% deposit now ranges from 2.7 years (Darwin unit) to 7.7 years (Sydney house). Brisbane now takes longer than Sydney for an entry-level unit, marking the first time it has overtaken Sydney on this measure.

- Housing Stress: Across all capitals, entry-level houses consume about 48.9% of income, well above the 30% stress benchmark, while units require ~30.9%. In regional areas, houses use 34.4% of income on repayments (units 26.9%).

- Unit Advantage: Units generally allow much faster entry. For many buyers, an apartment or townhouse means tens of months less saving, since both the price and loan repayments are lower than for houses.

- Government Support: New schemes are helping. The expanded 5% Deposit Scheme (no lender’s mortgage insurance) can cut saving time by over 5 years for eligible buyers. The Help-to-Buy equity scheme also stretches purchasing power (Govt can chip in up to 40% on new builds).

What This Means for First-Home Buyers

These trends aren’t a short-term blip but a structural shift – home prices have outpaced incomes for years. It’s now harder than ever to reach that first home, especially in big cities. However, as buyer’s agents, we also see opportunity in strategy and diversity. Growth has been fastest in Brisbane, Adelaide and Perth – keeping an eye on these markets (and local supply constraints) can pay off. In contrast, Canberra and Melbourne entry-level markets are relatively more stable, giving wage growth more breathing room.

It’s also time to make the most of support schemes. Governments have expanded deposit help (5% deposit guarantee) and equity schemes to speed entry. We help clients navigate these programs and structure purchases (such as leveraging the First Home Buyer Grant or stamp duty exemptions) to cut years off the savings timeline.

Our advice at D’MANSHA is to turn these numbers into a clear plan. We help you weigh up suburbs, property types and loan options so you enter on the right foot. Whether it’s skipping to a unit, choosing a cheaper city, or using a deposit scheme, a smart strategy is key. Another approach may be to step away from the grants available in your home state and explore acquiring an investment property interstate.

For one-on-one guidance, call us on 0406 11 22 44 or book a free consultation. We’ll help you make sense of the data, refine your search, and use grants or schemes to your advantage. For more insights, follow us on LinkedIn and Instagram.