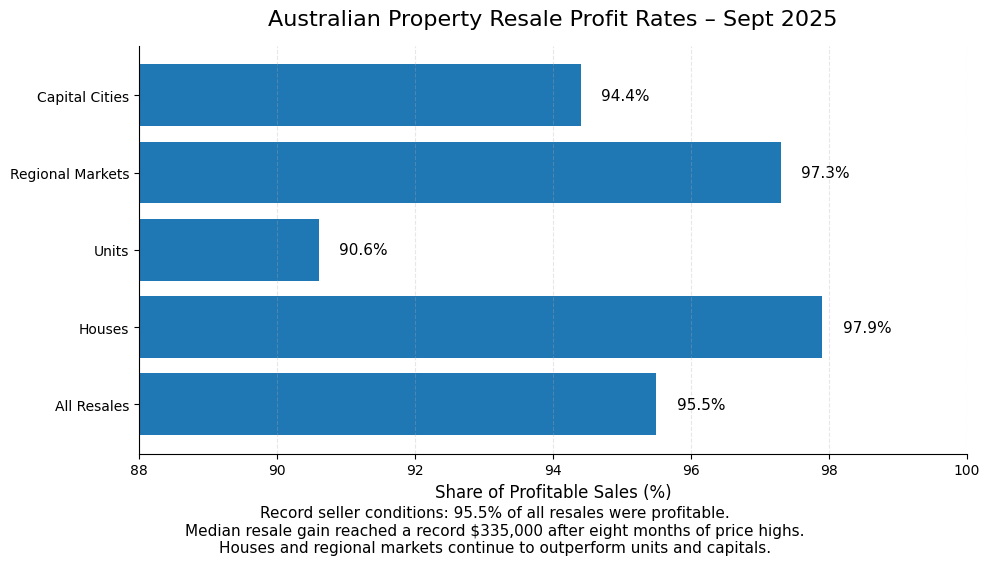

As we move into 2026, the latest available data shows Australian homeowners are still sitting on substantial gains. According to property analytics firm Cotality, 95.5% of homes resold for a profit in the most recently reported quarter (September 2025) — the highest share since 2005. The median resale gain reached a record $335,000, following eight consecutive months of rising national home values through 2025, supported in part by earlier rate cuts and improved credit conditions.

- 95.5% of resales profitable (highest since 2005).

- Median gain $335,000 – a record high, up from $325,600 in 2021.

- Home prices at record highs: Values set new peaks for 8 months in a row.

- Houses vs. Units: Around 98% of houses will earn a profit compared to 91% of units; however, units account for 69% of all losses.

- Regional Growth: 97.3% of all sold properties in regions will earn a profit compared with 94.4% for properties sold in capital cities.

As a Sydney based buyer’s agency, we see big implications for home buyers and mortgage brokers. On one hand, many owners now have extra equity – great news for financing an upgrade or investment. On the other hand, this boom raises warnings for recent buyers. Prices are high, and Cotality warns the 2026 outlook is uncertain as interest rates bite. We encourage everyone to stress-test their budgets and keep a safety buffer.

Key Takeaways for Buyers and Brokers

- Leverage equity growth: With strong resale profits, many owners can tap extra equity for their next purchase. Brokers should help clients calculate their new borrowing power (try our Calculators page) and look for upgrade or portfolio opportunities.

- Beware of rate shifts: The future path of interest rates is unclear. New loans should include a buffer – consider fixing or extra repayments. For example, try our Loan Repayment Calculator to compare interest-only vs principal-and-interest scenarios.

- Review loan structure: If a client is on an interest-only loan, check if that still makes sense. Switching to principal-and-interest can lock in equity as rates rise. In our How We Work approach, we regularly review loan terms with buyers to maximise benefit.

- Unit vs House risk: Units had a higher loss rate, so make sure any apartment purchase is conservatively priced and serviced. (See our Who We Work With section on different buyer needs.) Detached houses have been safer bets this cycle.

- Regional vs Metro: Regional markets showed slightly higher profit rates than Metro. If your strategy allows, consider growth in some regional areas; for capital cities, note local differences (Brisbane led profitability at 99.8%).

- Maintain buffers: We advise borrowing below the maximum. A 0.5–1% cushion for higher rates can protect against future stress. Even clients with healthy equity benefit from a safety margin if rates rebound in 2026.

Staying ahead of these market shifts is our job at D’MANSHA. Our data-driven process turns statistics like these into strategy. Ready to talk strategy? Call us on 0406 11 22 44 or book a free discovery call to chat with our team. We’ll walk you through the numbers and make sure your plan suits this market’s ups and downs. Also, follow us on LinkedIn and Instagram to stay updated with the latest market trends.