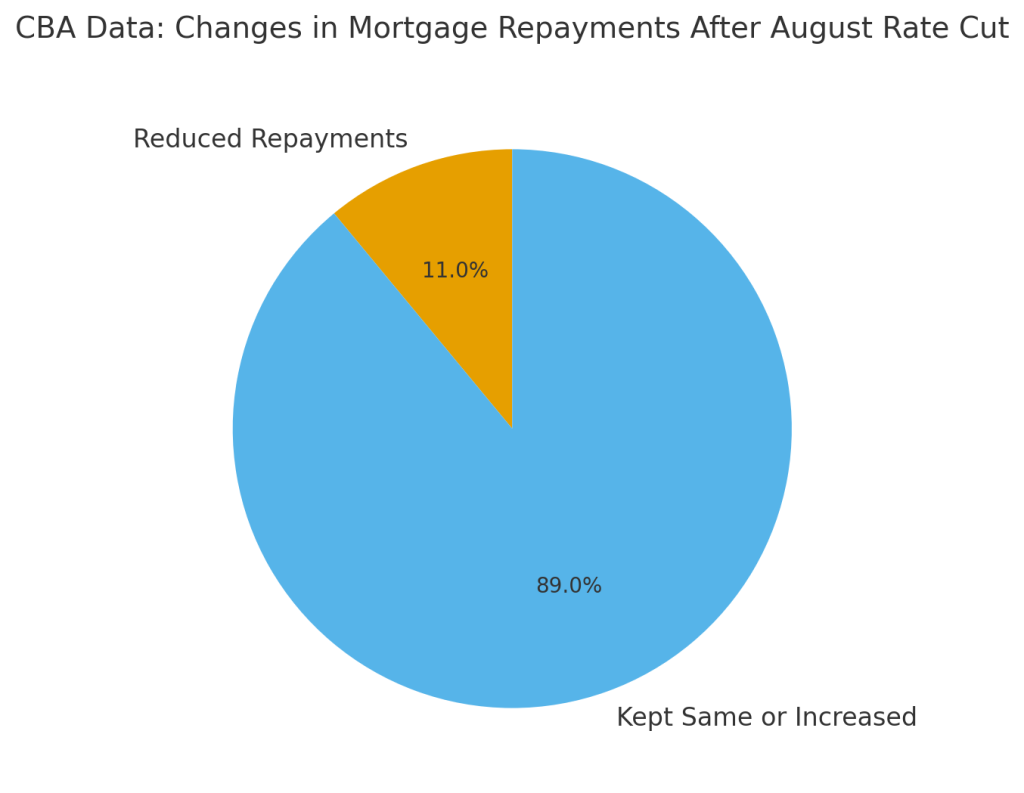

The recent rate‑cut decision by the Reserve Bank triggered a telling shift in the way Australians manage their mortgage repayments. New data from the Commonwealth Bank of Australia (CBA) shows that 11 % of eligible customers reduced their direct debit repayments after the August rate cut. Understanding who is making these changes and why helps us, as buyer’s agents, guide our clients through today’s evolving property market.

How Different Age Groups Are Adjusting Their Loan Repayments

Data from the CBA suggests that the public is responding to rising living costs in different ways. Many are reducing their home loan repayments, particularly people in their 30s and 40s, who tend to have the biggest family outgoings. Here’s how the repayment reliefs are split out by age group:

| Age Group | Borrowers Who Cut Repayments |

| Under 20 years | 8% |

| 21–30 years | 11% |

| 31–40 years | 14% |

| 41–50 years | 13% |

| 51–60 years | 9% |

| Over 60 years | 7% |

| First-home buyers | 8% |

CBA notes that 30- and 40-year-olds are the most likely to seek repayment relief, as they juggle mortgages, family costs, and day-to-day expenses.

As your buyer’s agent in Sydney, we interpret these figures to gauge buyer sentiment — younger and mid-career borrowers are looking for flexibility and short-term relief, while older borrowers tend to stay the course with steady repayments.

State‑level trends are similar: New South Wales and the ACT top the list at 14 %, with Victoria at 12 % and Queensland and South Australia at 9 %. Northern Territory, Western Australia and Tasmania saw 7 %. With three cuts over the past year, a borrower on a $500,000 principal‑and‑interest loan saves around $240 per month, money that can ease budgets or be reinvested.

Implications for buyers and investors

As a buyers agent in Sydney, we see that 30‑ and 40‑something borrowers freeing up cash flow will keep pressure on family homes, while the restraint of older borrowers suggests stability in downsizer markets. Key takeaways include:

- Competition mapping – Expect strong demand in family suburbs. We monitor listings, auction trends and leverage off‑market opportunities via our How We Work process.

As your buyers agent in Sydney, we ensure you’re aware of this competition. - Suburb targeting – Prioritise rising‑listing pockets rather than overcrowded hotspots. Our Process helps identify value early.

- Deal tactics – Secure pre‑approval and consider early offers with clean terms. Our Who We Work With page shows how we tailor strategies.

Working with a buyers agent in Sydney can provide the edge in negotiations. - Risk and cash flow – Include finance and inspection clauses, check bank valuations and maintain a buffer by stress‑testing at current and higher rates.

A recovering economic backdrop

CBA economists note that households are benefiting from lower inflation, rate cuts and tax changes, with six months of improved spending momentum. This stability should support property values, though some clients prefer to keep repayments steady to build equity. Our role as a buyer’s agent in Sydney is to tailor advice to your circumstances.We at D’MANSHA can guide you. If you’re ready to take the next step, call us on 0406 11 22 44 or book a free strategy session. As a buyer’s agent in Sydney, we’ll help you stress‑test your budget, pick the right suburbs and negotiate effectively.